Audit Firm Registration Process

Audit Firm Registration Process

“Pursuant to Part IXC of SECP Act, 1997 and regulations made thereunder, it is of critical importance that auditors are registered with AOB before giving consent or accepting any appointment as auditor of a Public Interest Company. For ease of reference, a presentation is prepared to assist the potential auditors of PICs with respect to their responsibilities and process of AOB registration. See attached.”

To get registered with the Audit Oversight Board (AOB), an audit firm is required to follow the procedure as laid down in sub-regulation 2 of regulation 4 of the Audit Oversight Board (Operations) Regulations, 2018 (the AOB Regulation). Here is a step-wise guidance to the procedure:

1. Prepare Form-A and Obtain Letter of Recommendation (LOR) QAB

(i) Complete Form-A as per schedule 2 the AOB Regulation.

(ii) Print Form-A and get it signed by the firm’s authorized audit partner, and affix the firm’s stamp.

(iii) Submit Form-A to QAB to obtain a LOR, as specified in Schedule 4 to the AOB Regulations.

2. Submission of Form-A and LOR to AOB

Once the LOR is received from QAB, please submit the LOR along with Form-A to AOB, in orignal.

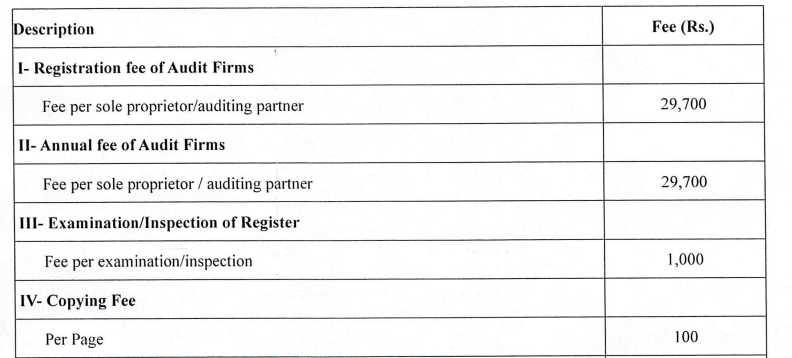

3. Fee Submission

A demand draft will be shared by AOB for payment of a applicable fee as specified in Schedule 3 to the AOB Regulation.

4. Certificate of Registration

Subject to regulation 4B, AOB may approve registration of an audit firm and in token of its approval, shall issue a Certificate of Registration under the signature of an Authorized Officer of AOB and enter the particulars of the applicant audit firm in the Register. A Certificate of Registration entitles the audit firm to conduct audit of public interest companies. The particulars of registered audit firm shall be entered in the Register which shall be posted on the website of AOB:

Provided that the registration of an audit firm shall be subject to continuing compliance with conditions stated below which require that firm shall be:

-

- maintaining satisfactory QCR Rating under the QCRF;

- complying with all the applicable laws and regulations, QCRF, International Standards on Auditing (ISAs), relevant requirements of code of ethics as adopted by Institute, international standards related to quality and other professional pronouncements as applicable in Pakistan, by the audit firm and its Audit Partners;

- submitting Form A as specified in Schedule 2 annually;

- timely depositing the specified annual Fee;

- submitting the revised Form A as specified in Schedule 2 to AOB within 15 days from the occurrence of changes, if any, in the particulars of registered audit firm;

- engaged as auditor of at least one public interest company during the last two consecutive calendar years, as reported in annual Form A; and

- ensuring compliance with all directives and orders passed under Sections 36CC or 36AA of the Act and these regulations, including paying and depositing the amount of any penalty in the Federal Consolidated Fund, unless the directives and orders are challenged through a representation filed under these regulations which is pending final adjudication or there is a restraining order from the Court under Section 36V of the Act.

Provided that an audit firm that is already registered with AOB shall ensure compliance with the above-said clause (vi) by 1 January 2025.